Annuity

Definition

An annuity is a financial product or arrangement involving a series of equal payments made at regular intervals over a fixed period or for the duration of a lifetime.

These payments can either be inflows (income received) or outflows (payments made), depending on the context:

Investment Annuity: Purchased through an insurer to receive future income.

Loan Annuity: Paid regularly to repay borrowed capital and interest.

Origins

The concept of annuities dates back to Roman times, where citizens purchased annua (Latin for “annual stipends”) from the state in return for annual payments. The modern financial annuity evolved with the development of life insurance and pension systems in the 17th–18th centuries in Europe, and gained traction as a retirement income product in the 20th century.

Usage

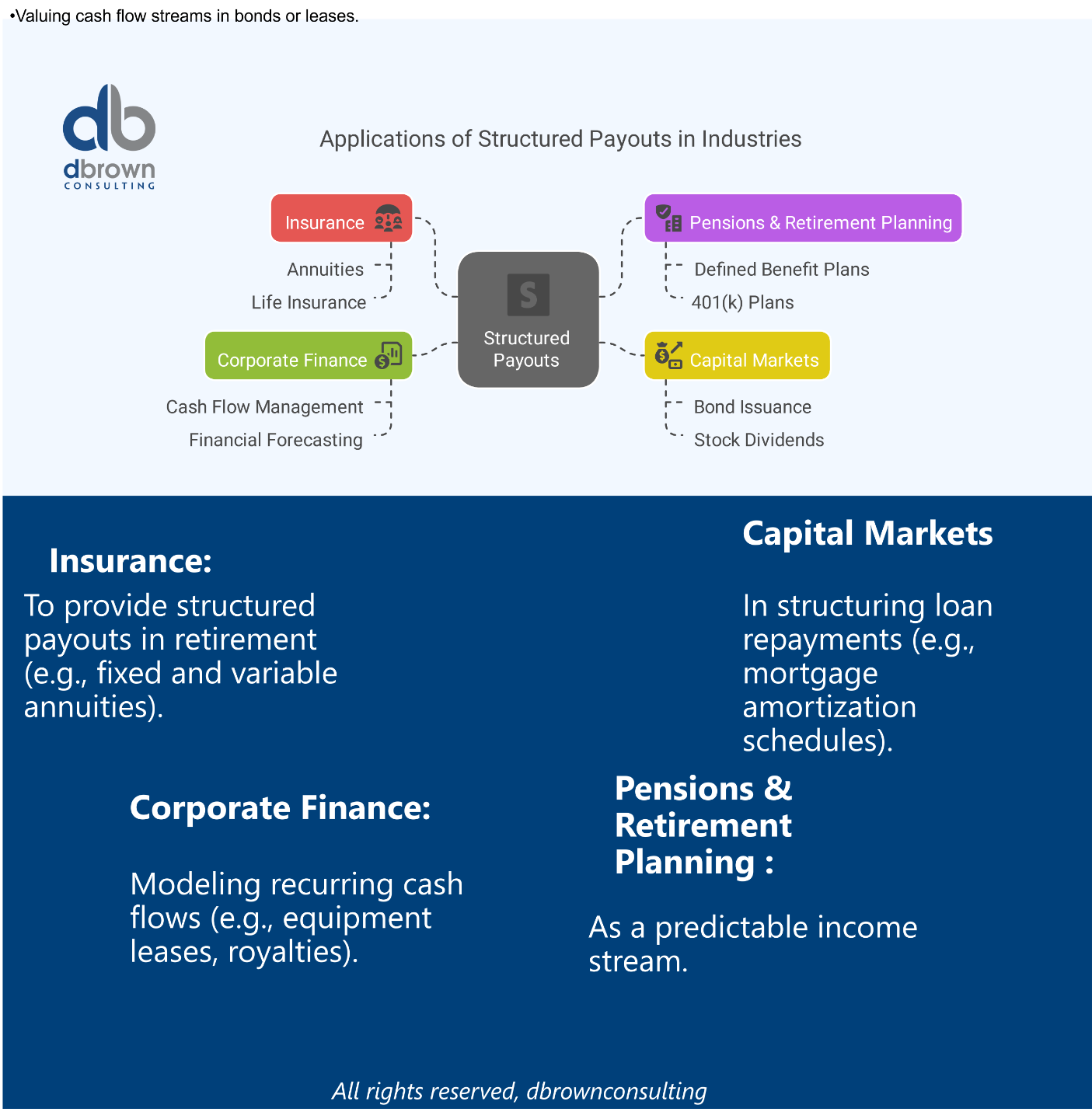

Industry Applications:

-

Insurance – To provide structured payouts in retirement (e.g., fixed and variable annuities).

-

Pensions & Retirement Planning – As a predictable income stream.

-

Capital Markets – Valuing cash flow streams in bonds or leases.

-

Corporate Finance – Modeling recurring cash flows (e.g., equipment leases, royalties).

How Market Inefficiency Works

An annuity involves:

A principal (initial investment or loan).

A fixed or variable interest rate.

A payment frequency (monthly, quarterly, annually).

A defined term or lifetime over which payments occur.

There are two core dimensions:

-

Timing:

-

Ordinary Annuity – Payments at end of each period.

-

Annuity Due – Payments at the beginning of each period.

-

-

Type:

-

Fixed – Known payment amounts.

-

Variable – Payments fluctuate based on investment performance.

-

Key Takeaways

-

Annuities provide predictable cash flows and reduce financial uncertainty.

Their value is based on the time value of money principle.

Used across retirement income planning, debt repayment, and financial modeling.

Differentiated by timing (ordinary vs. due) and structure (fixed, variable, immediate, deferred).

Types & Variations of Market Inefficiency

| Type | Description |

|---|---|

| Fixed Annuity | Pays a guaranteed, fixed amount over time. |

| Variable Annuity | Payout varies based on investment returns. |

| Immediate Annuity | Begins payout shortly after investment. |

| Deferred Annuity | Begins payout at a future date. |

| Ordinary Annuity | Payments at the end of the period. |

| Annuity Due | Payments at the beginning of the period. |

| Perpetuity | A special annuity that pays indefinitely. |

Context in Financial Modeling

Annuities appear in many modeling contexts:

-

DCF Valuation: Forecasting regular cash inflows (e.g., rental income).

-

Bond Valuation: Coupon payments are modeled as annuities.

-

Loan Modeling: Loan payments use annuity formulas to amortize debt.

-

Lease Modeling: IFRS 16 / ASC 842 requires modeling leases as annuities.

They are used to:

-

Forecast stable cash flows

-

Evaluate NPV and IRR

-

Estimate future values or present values

Nuances & Complexities

-

-

Tax Implications: Taxation differs by country and annuity type (investment vs pension).

-

Inflation Risk: Fixed annuities lose value in inflationary environments.

-

Longevity Risk: Annuities mitigate outliving retirement savings.

-

Fee Structures: Variable annuities may include high fees and surrender charges.

-

Mathematical Formulas

Present Value of Ordinary Annuity:

2. Future Value of Ordinary Annuity:

3. For Annuity Due:

Multiply result by

Where:

-

= payment amount per period

-

= interest rate per period

-

= total number of periods

Master Financial Modeling with the FMA

Change your career today by earning a Globally Recognized Accreditation

Develop real-world financial modeling skills, gain industry-recognized expertise, stand out and start earning more by gaining the Advanced Financial Modeler (AFM) designation from the Financial Modeling Institute.

Our expert-led online cohort based program covers everything you need to become a world class financial modeling pro and advance your career in finance.

Related Terms

-

Perpetuity

-

Amortization

-

Time Value of Money (TVM)

-

Present Value (PV)

-

Future Value (FV)

-

Bond Yield

-

Lease Payments

Real-World Applications

Retirement Planning

A retiree invests $500,000 into a fixed immediate annuity and receives $2,500/month for life, mitigating longevity risk.

2. Loan Repayment Modeling

A $100,000 loan over 10 years at 6% is repaid via monthly annuity payments. Each payment includes principal + interest.

3. Lease Accounting

Under IFRS 16, a 5-year lease with fixed payments of $10,000 annually is modeled as a present value of an annuity, affecting both assets and liabilities.

References & Sources

Unlock the Language of Finance!

Elevate your financial acumen with DBrown Consulting’s exclusive newsletter. We break down complex finance terms into clear, actionable insights—empowering you to make smarter decisions in today’s markets.

Subscribe Today & Make Financial Jargon Simple!

We won't send spam. Unsubscribe at any time.