Goodwill

Definition

Goodwill is an intangible asset that arises when a company acquires another business for more than the fair value of its identifiable net assets (i.e., assets minus liabilities). It represents the future economic benefits from assets not individually identified or separately recognized.

In simple terms:

Goodwill = Purchase Price – Fair Value of Net Identifiable Assets

Origins

The concept of goodwill dates back to 19th-century accounting, where it was informally recognized as the premium paid for customer relationships, brand value, or management strength. With the growth of mergers and acquisitions, accounting standards formalized its treatment:

- U.S. GAAP (ASC 805/350)

- IFRS (IFRS 3 / IAS 36)

Usage

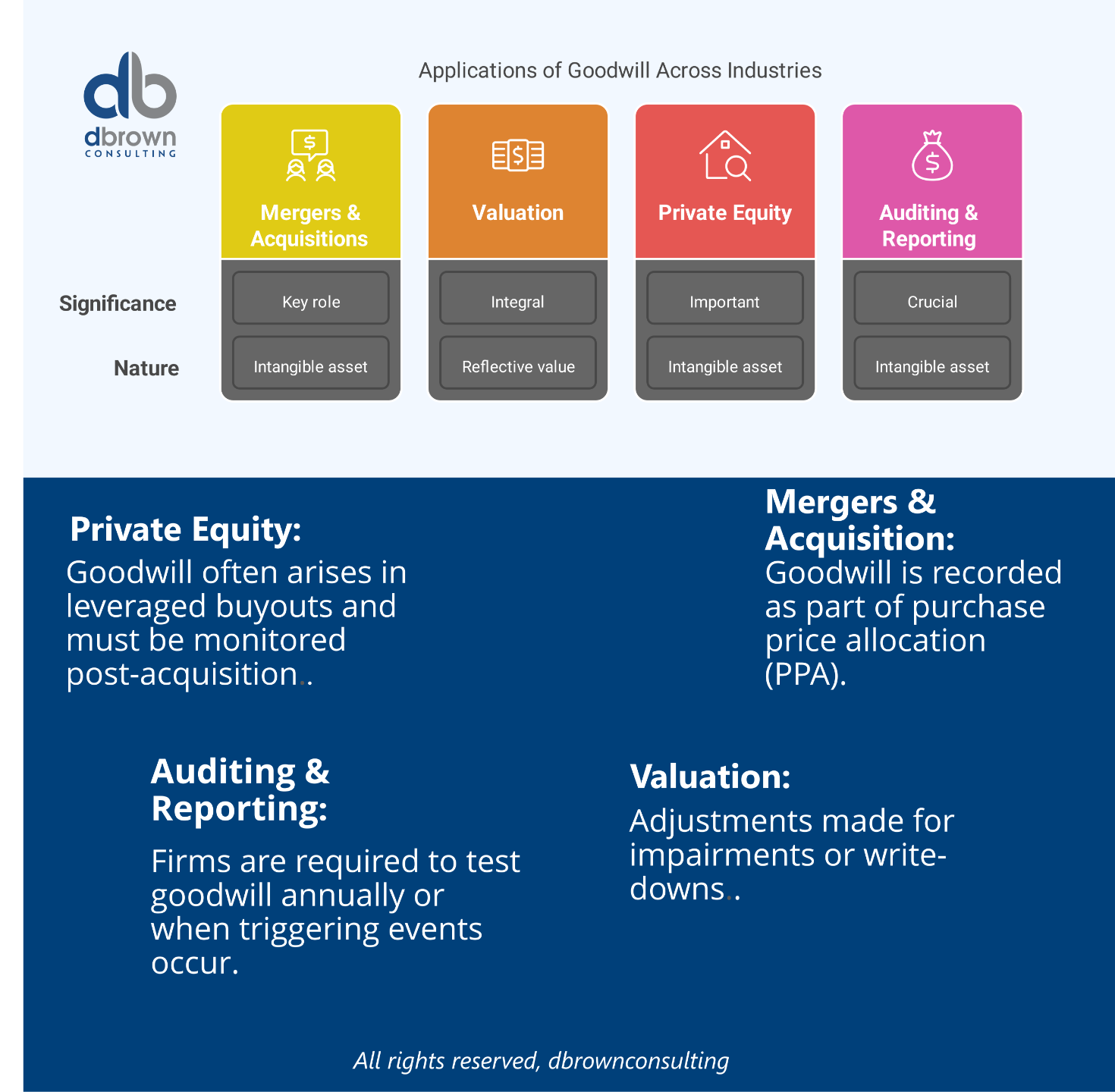

Industry Applications:

-

Mergers & Acquisitions – Goodwill is recorded as part of purchase price allocation (PPA).

-

Valuation – Adjustments made for impairments or write-downs.

-

Private Equity – Goodwill often arises in leveraged buyouts and must be monitored post-acquisition.

-

Auditing & Financial Reporting – Firms are required to test goodwill annually or when triggering events occur.

How Goodwill Works

1. Acquisition Accounting (PPA)

- After acquiring a company, the acquirer:

- Allocates purchase price to fair value of identifiable assets/liabilities.

- Any excess is booked as goodwill on the balance sheet.

2. Post-Acquisition Treatment

- Goodwill is not amortized under IFRS or U.S. GAAP.

- Subject to annual impairment testing (or more frequently if indicators exist).

- Impairment occurs when carrying value > recoverable value.

Key Takeaway

-

Goodwill reflects intangible value such as brand, reputation, and synergies.

-

It only arises from business combinations—not internally developed.

-

Not amortized, but tested for impairment, potentially affecting earnings.

-

Appears as a non-current intangible asset on the balance sheet.

-

Does not generate cash flows independently.

Types of Goodwill

Type |

Description |

|---|

| Purchased Goodwill | Arises in acquisitions; recognized on balance sheet. |

| Internally Generated | Not recognized under GAAP/IFRS; arises from organic growth. |

| Positive Goodwill | Purchase price exceeds fair value of net assets (most common). |

| Negative Goodwill | Fair value > purchase price (treated as a bargain purchase gain under IFRS/GAAP). |

Context in Financial Modeling

Goodwill plays a major role in:

-

M&A Modeling:

-

Recorded during purchase price allocation.

-

Impairment modeled under synergy failure or valuation decline.

-

-

DCF Valuation:

-

Excluded from cash flows, but impairment affects EBIT, taxes, and net income.

-

-

Balance Sheet Modeling:

-

Appears under intangible assets.

-

Tracked for potential impairment charges.

-

Common modeling steps:

-

Model goodwill creation during M&A.

-

Forecast no amortization.

-

Model impairment loss scenarios as non-cash adjustments to earnings.

Nuances & Complexities

-

Impairment Risk: Overpayment in M&A can result in massive goodwill write-downs.

-

Non-Cash Nature: Goodwill doesn't impact cash flow unless impaired.

-

Judgment-Heavy: Impairment testing involves significant assumptions (discount rate, growth).

-

Audit Scrutiny: Firms with high goodwill balances face extra scrutiny.

-

Negative Goodwill: Rare, but reflects a bargain purchase; recorded as income immediately.

Mathematical Formulas

1. Goodwill Calculation:

2. Impairment Test (GAAP/IFRS):

-

Recoverable Amount = higher of Value in Use (DCF) or Fair Value less Costs to Sell

Master Financial Modeling with the FMA

Change your career today by earning a Globally Recognized Accreditation

Develop real-world financial modeling skills, gain industry-recognized expertise, stand out and start earning more by gaining the Advanced Financial Modeler (AFM) designation from the Financial Modeling Institute.

Our expert-led online cohort based program covers everything you need to become a world class financial modeling pro and advance your career in finance.

Related Terms

-

Intangible Assets

-

M&A Accounting (ASC 805 / IFRS 3)

-

Impairment (ASC 350 / IAS 36)

-

Purchase Price Allocation (PPA)

-

Enterprise Value

-

Synergies

-

Bargain Purchase

Real-World Applications

1. Goodwill in M&A

When Microsoft acquired LinkedIn for ~$26B, over $15B was allocated to goodwill, reflecting brand, user base, and growth potential not recognized on LinkedIn’s balance sheet.

2. Impairment Example

In 2020, General Electric took a $22B goodwill impairment due to lower growth forecasts in its power division.

3. Private Equity Use

A PE firm acquires a portfolio company and books $200M of goodwill. Impairment is tested yearly using a DCF-based valuation for each reporting unit.

References & Sources

Unlock the Language of Finance!

Elevate your financial acumen with DBrown Consulting’s exclusive newsletter. We break down complex finance terms into clear, actionable insights—empowering you to make smarter decisions in today’s markets.

Subscribe Today & Make Financial Jargon Simple!

We won't send spam. Unsubscribe at any time.