-

Surety

-

Collateral

-

Co-Signer

-

Contingent Liability

-

Credit Enhancement

-

Letter of Credit

-

Loan Covenant

-

Recourse vs. Non-Recourse Debt

Real-World Applications

1. SME Loan with Personal Guarantee

A small business obtains a $500,000 loan. The owner signs a personal guarantee, making them liable in case of default—even if the business is a separate legal entity.

2. Corporate Parent Guarantee

A multinational’s parent company issues a corporate guarantee for its overseas subsidiary's bond issue to achieve an investment-grade credit rating.

3. Sovereign Guarantees

In a World Bank-financed power project, the host government acts as a sovereign guarantor, ensuring loan repayment in case of project failure.

4. Bank Guarantees in Construction

A construction firm wins a government tender with a bank guarantee ensuring contract fulfillment and performance.

GUARANTOR

Definition

A guarantor is a third party who agrees to take responsibility for a borrower’s debt or obligation if the borrower defaults. The guarantor provides a financial backstop, improving the creditworthiness of the borrower in the eyes of the lender.

In essence:

A guarantor assures the lender that if the primary obligor fails to repay, they will step in.

Origins

The practice of guaranteeing obligations dates back to ancient commercial law, where merchants relied on third-party guarantees for long-distance trade. In modern finance, guarantees have become a formal legal tool, governed by contract law, banking regulations, and credit risk frameworks.

Usage

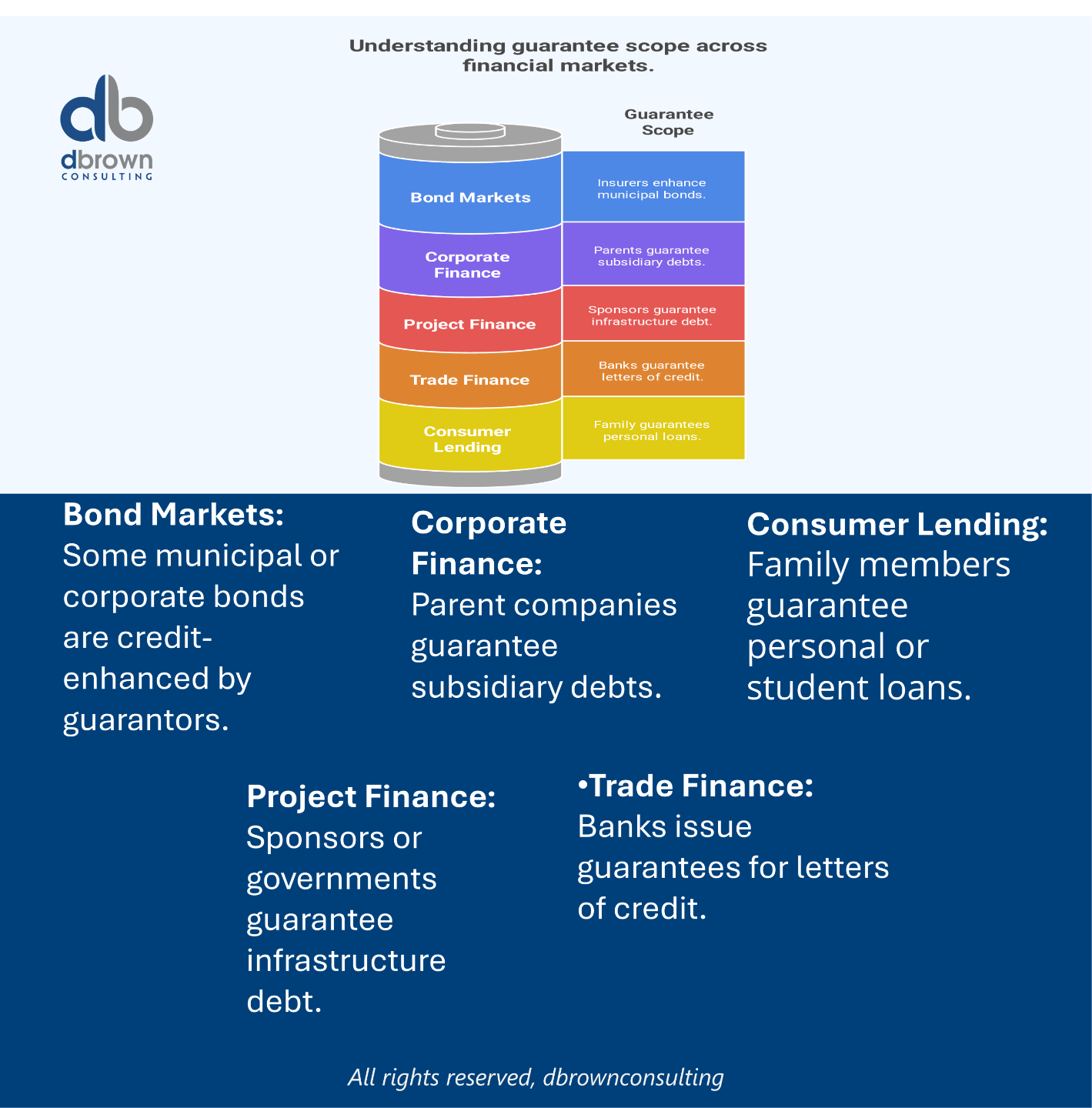

Industry Applications:

-

Corporate Finance – Parent companies guarantee subsidiary debts.

-

Consumer Lending – Family members guarantee personal or student loans.

-

Project Finance – Sponsors or governments guarantee infrastructure debt.

-

Trade Finance – Banks issue guarantees for letters of credit.

-

Bond Markets – Some municipal or corporate bonds are credit-enhanced by guarantors (e.g., insurance firms).

How Guarantor works

Mechanics of a Guarantee:

- A guarantee agreement is signed between the lender and the guarantor.

- It can be:

- Unconditional (payment must be made on demand).

- Conditional (obligation triggered only after legal action against the borrower).

- The guarantor becomes jointly or severally liable for repayment.

Types of Guarantees:

-

Personal Guarantee – Often seen in SME lending.

-

Corporate Guarantee – Parent entity guarantees subsidiary liabilities.

-

Bank Guarantee – Common in trade and construction contracts.

- Performance Guarantee – Ensures fulfillment of a contract or service.

Key Takeaways

-

A guarantor mitigates credit risk for lenders.

-

It can enable better loan terms, such as lower interest rates or higher limits.

-

The guarantor bears secondary liability—activated only upon borrower default.

-

Can expose the guarantor to full financial risk if not carefully structured.

Types of Guarantors

| Type | Description |

|---|---|

| Individual Guarantor | A person guarantees another’s debt (e.g., parent-student loan). |

| Corporate Guarantor | A company guarantees a loan for an affiliate or subsidiary. |

| Sovereign Guarantor | A government backs obligations (common in infrastructure). |

| Bank Guarantor | A bank guarantees payments (e.g., standby letters of credit). |

Guarantors & Financial Modeling

While guarantors don’t directly alter cash flows, they impact:

-

Credit risk assessments (i.e., default risk reduction).

-

Debt pricing—guaranteed loans may carry lower interest.

-

Covenants—may trigger financial ratios inclusive of guarantor’s balance sheet.

-

Off-Balance Sheet Exposure—may require disclosure in contingent liabilities.

-

Scenario Analysis—modeling if guarantor needs to assume liability.

Example: In a project finance model, if the project company defaults, the sponsor-guarantor's financial model must reflect the obligation.

Nuances & Complexities

-

Not Always Recognized On-Balance Sheet: Guarantors may disclose guarantees in footnotes unless liability becomes probable.

-

Moral Hazard: Borrowers may take on more risk if backed by strong guarantors.

-

Legal Risks: Enforceability depends on jurisdiction, contract specificity, and guarantee terms.

-

Cross-Default Risk: A guarantee may trigger defaults across other obligations.

-

Credit Rating Agencies: May consolidate guaranteed debt into the guarantor’s analysis.

Mathematical Formulas

-

1. Credit Risk Assessment Adjustments:

2. Guarantor Exposure Calculation:

3. Leverage Implications for Guarantor:

Master Financial Modeling with the FMA

Change your career today by earning a Globally Recognized Accreditation

Develop real-world financial modeling skills, gain industry-recognized expertise, stand out and start earning more by gaining the Advanced Financial Modeler (AFM) designation from the Financial Modeling Institute.

Our expert-led online cohort based program covers everything you need to become a world class financial modeling pro and advance your career in finance.

Unlock the Language of Finance!

Elevate your financial acumen with DBrown Consulting’s exclusive newsletter. We break down complex finance terms into clear, actionable insights—empowering you to make smarter decisions in today’s markets.

Subscribe Today & Make Financial Jargon Simple!

We won't send spam. Unsubscribe at any time.