Hedge Funds

Definition

A hedge fund is a pooled investment vehicle that uses a wide range of strategies to generate returns for its investors. These strategies may include leveraging, short selling, derivatives, arbitrage, and event-driven investing. Unlike mutual funds, hedge funds are lightly regulated, have restricted investor access, and often aim for absolute returns regardless of market conditions.

Origins

The first hedge fund was created in 1949 by Alfred Winslow Jones, who combined long stock positions with short sales to "hedge" against market downturns—hence the name. Over time, hedge funds evolved into complex, high-risk, high-reward vehicles. In the 1990s and 2000s, major funds like Long-Term Capital Management (LTCM) and Bridgewater Associates shaped how hedge funds are perceived and regulated.

Usage

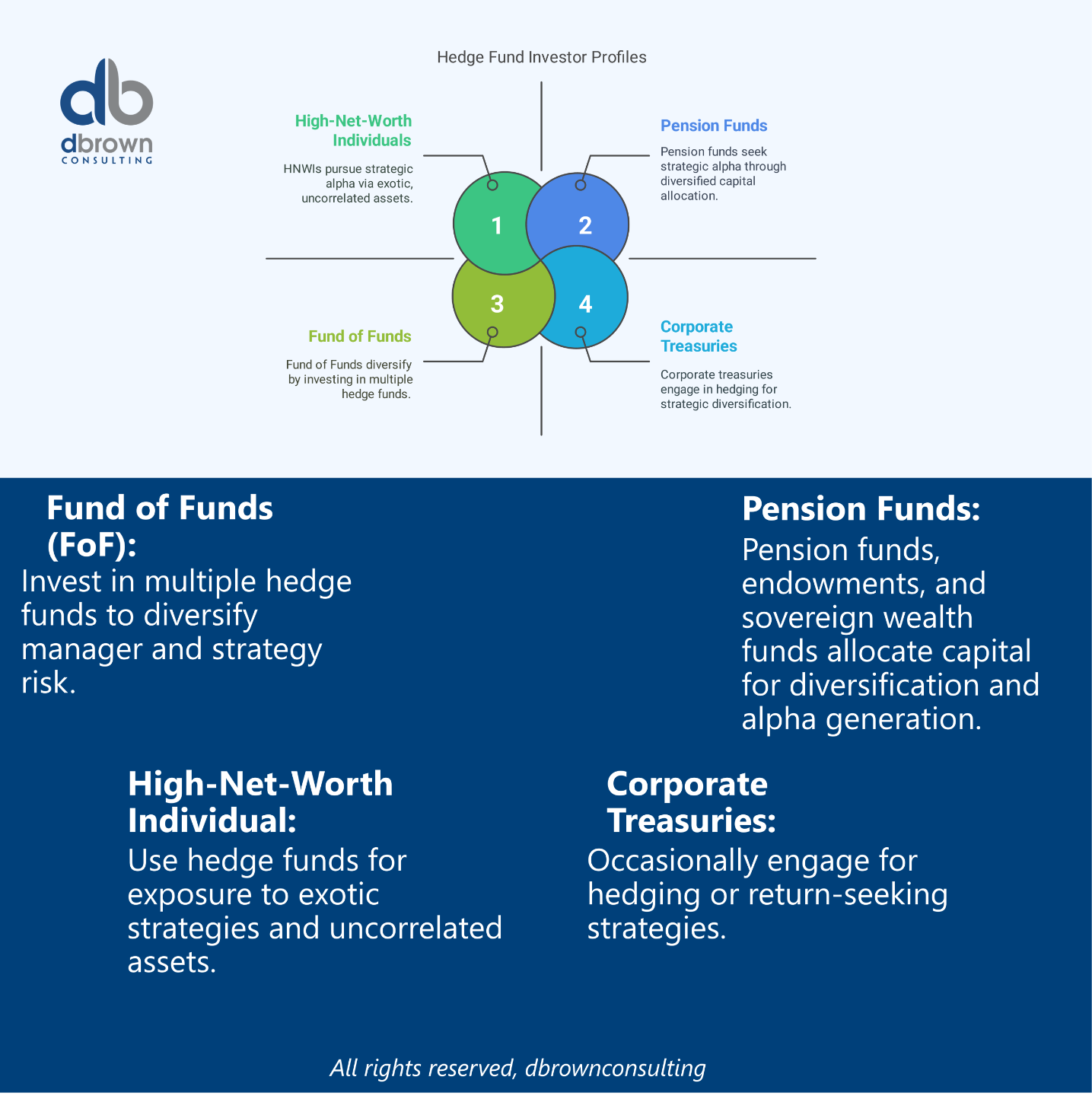

Industry Applications:

-

Institutional Investors – Pension funds, endowments, and sovereign wealth funds allocate capital for diversification and alpha generation.

-

High-Net-Worth Individuals (HNWIs) – Use hedge funds for exposure to exotic strategies and uncorrelated assets.

-

Fund of Funds (FoF) – Invest in multiple hedge funds to diversify manager and strategy risk.

-

Corporate Treasuries – Occasionally engage for hedging or return-seeking strategies.

How Hedge Funds works

A hedge fund typically follows this structure:

-

Fund Manager (General Partner) – Operates the fund and executes strategies.

-

Investors (Limited Partners) – Provide capital and share in returns.

-

Fee Model – Usually “2 and 20”: 2% management fee + 20% performance fee.

-

Lock-Up Periods – Capital may be illiquid for months or years.

-

High Water Marks – Prevent managers from earning performance fees on past losses.

They deploy active management, with full flexibility in asset selection, geography, leverage, and risk.

Key Takeaways

-

-

Hedge funds pursue absolute returns, not just outperforming benchmarks.

-

Access is typically limited to accredited investors due to risk.

-

Strategies span a wide spectrum—from market-neutral to highly directional.

-

Risk and leverage are central to most hedge fund strategies.

-

Not regulated like mutual funds or ETFs (exempt from SEC registration under Reg D or Section 3(c)(7) exemptions).

-

Types & Variations of Hedge Funds

| Strategy Type | Description |

|---|

| Long/Short Equity | Buys undervalued stocks, shorts overvalued ones. |

| Global Macro | Trades across asset classes based on macroeconomic trends. |

| Event-Driven | Profits from mergers, bankruptcies, restructurings. |

| Relative Value Arbitrage | Exploits pricing inefficiencies between securities. |

| Quantitative/Systematic | Uses algorithms and data to drive decisions. |

| Distressed Securities | Invests in companies under financial duress. |

| Multi-Strategy | Combines several strategies to reduce volatility. |

| Market Neutral | Seeks uncorrelated returns by hedging beta. |

Context in Financial Modeling

In financial models:

Portfolio Allocation Models may include hedge funds as an asset class for risk-adjusted return enhancement.

Monte Carlo simulations assess hedge fund return distributions.

Stress Testing applies to liquidity, counterparty, and market shocks.

Used in Value-at-Risk (VaR) and Expected Shortfall modeling.

Alpha vs Beta Attribution separates skill-based return (alpha) from market exposure (beta).

Nuances & Complexities

-

-

Transparency: Hedge funds often provide limited disclosure.

-

Liquidity: Monthly or quarterly redemption windows, with notice periods.

-

Valuation: Illiquid assets may be marked to model.

-

Fees: Can be high and controversial, especially if performance lags.

-

Regulatory Risk: Subject to increasing global oversight post-2008 crisis.

-

Survivorship Bias: Performance databases often exclude failed funds.

-

Mathematical Formulas

1. Gross & Net Exposure:

2. Sharpe Ratio:

Where:

-

: Portfolio return

-

: Risk-free rate

-

: Standard deviation of returns

3. Alpha (Jensen’s Alpha):

-Water Mark:

Prevents performance fees until NAV exceeds previous peak.

Master Financial Modeling with the FMA

Change your career today by earning a Globally Recognized Accreditation

Develop real-world financial modeling skills, gain industry-recognized expertise, stand out and start earning more by gaining the Advanced Financial Modeler (AFM) designation from the Financial Modeling Institute.

Our expert-led online cohort based program covers everything you need to become a world class financial modeling pro and advance your career in finance.

Related Terms

-

Private Equity

-

Alternative Investments

-

Alpha & Beta

-

Leverage

-

Arbitrage

-

Fund of Funds

-

Accredited Investor

Real-World Applications

1. Bridgewater’s Global Macro Strategy

Uses macroeconomic models and risk parity to trade global bonds, currencies, and equities based on economic themes.

2. Long-Term Capital Management (LTCM)

Failed due to excessive leverage and liquidity mismatch, requiring a Fed-led bailout in 1998.

3. Institutional Portfolio Diversification

Yale Endowment allocates over 25% of its assets to hedge funds, citing low correlation with public equities.

References & Sources

Unlock the Language of Finance!

Elevate your financial acumen with DBrown Consulting’s exclusive newsletter. We break down complex finance terms into clear, actionable insights—empowering you to make smarter decisions in today’s markets.

Subscribe Today & Make Financial Jargon Simple!

We won't send spam. Unsubscribe at any time.