FORWARD CONTRACT

Definition

A forward contract is a customized, over-the-counter (OTC) agreement between two parties to buy or sell an asset at a predetermined price on a specified future date. Unlike exchange-traded futures, forwards are privately negotiated and can be tailored to fit the quantity, delivery date, and settlement terms agreed upon by both parties.

Forwards are widely used for hedging and speculating in foreign exchange, commodities, interest rates, and other markets.

Origins

The concept of forward trading dates back centuries, historical records from the Osaka Rice Exchange in 17th-century Japan and Dutch tulip markets in the 1600s describe similar agreements. The term forward refers to setting a transaction for a future (forward) date rather than immediate settlement.

Usage

-

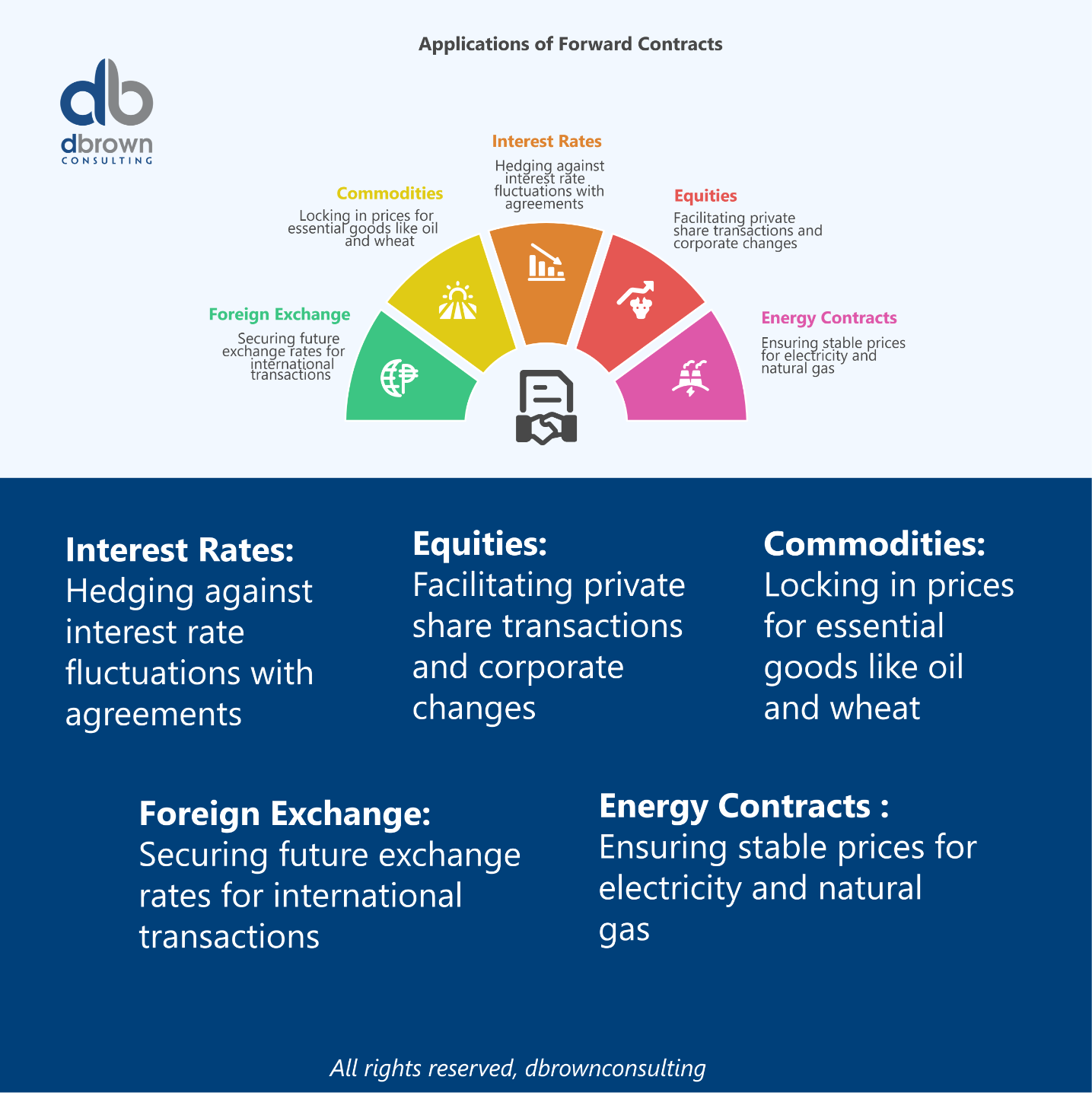

Foreign Exchange (FX) – Lock in exchange rates for future payments.

-

Commodities – Secure supply or sales prices in advance (e.g., oil, wheat).

-

Interest Rates – Hedge against fluctuations with forward rate agreements.

-

Equities – Used in private share transactions or corporate restructuring.

-

Energy Contracts – Lock in electricity or natural gas prices.

How a Forward Contract Works

-

Agreement – Two parties negotiate the asset, quantity, price, and settlement date.

-

No Initial Payment – Typically no money changes hands at inception.

-

Obligation – Both buyer and seller must perform at maturity, regardless of market price.

-

Settlement – Can be physical delivery or cash settlement based on price differences.

-

Credit Risk – Counterparty default is a key concern since forwards are OTC.

Types of Forward Contracts

-

Deliverable Forward – Physical delivery of the underlying asset at maturity.

-

Non-Deliverable Forward (NDF) – Cash-settled based on price difference.

-

Flexible Forward – Allows delivery anytime within a set range of dates.

-

Window Forward – Settlement possible within an agreed window period.

Key Takeaway

-

OTC and customizable – Flexible contract terms.

-

Binding obligation – Both parties must execute regardless of price changes.

-

Used for hedging and speculation – Lock in prices or bet on price movements.

-

Credit risk exposure – Unlike exchange-traded futures, there’s no clearinghouse guarantee.

Context in Financial Modeling

Forward contracts are modeled for:

-

Hedging strategies – Locking input/output prices in commodity-based businesses.

-

FX exposure management – Predicting and mitigating currency fluctuations.

-

Interest rate forecasting – Using forward rates in bond pricing.

-

Risk-adjusted valuations – Incorporating forward curves into discounted cash flow models.

Nuances & Complexities

-

Mark-to-Market Risk – Daily valuation changes impact credit exposure.

-

Liquidity Risk – Customization reduces marketability.

-

Regulatory Oversight – Post-2008 reforms increased reporting requirements.

-

Hedging Inefficiencies – Basis risk may occur if forward price doesn’t perfectly track exposure.

Mathematical Formulas

The theoretical forward price () for a non-dividend-paying asset:

Where:

-

= Spot price of the asset

-

= Risk-free interest rate (continuously compounded)

-

= Time to maturity (in years)

For discrete compounding:

For currency forwards:

Where is the domestic interest rate and is the foreign interest rate.

Master Financial Modeling with the FMA

Change your career today by earning a Globally Recognized Accreditation

Develop real-world financial modeling skills, gain industry-recognized expertise, stand out and start earning more by gaining the Advanced Financial Modeler (AFM) designation from the Financial Modeling Institute.

Our expert-led online cohort based program covers everything you need to become a world class financial modeling pro and advance your career in finance.

Related Terms

-

Futures Contract

-

Spot Price

-

Hedging

-

Basis Risk

-

Counterparty Risk

-

Forward Rate Agreement (FRA)

Real-World Applications

Example 1: FX Forward

An importer agrees to buy €1M in 90 days at $1.10/€, protecting against euro appreciation.

Example 2: Commodity Forward

A wheat producer locks in $6.50/bushel for a harvest due in six months, eliminating price uncertainty.

Example 3: NDF

A company operating in a restricted currency market (e.g., INR/USD) uses an NDF to hedge without physical currency delivery.

References & Sources

Unlock the Language of Finance!

Elevate your financial acumen with DBrown Consulting’s exclusive newsletter. We break down complex finance terms into clear, actionable insights—empowering you to make smarter decisions in today’s markets.

Subscribe Today & Make Financial Jargon Simple!

We won't send spam. Unsubscribe at any time.