HOLDING COMPANY

Definition

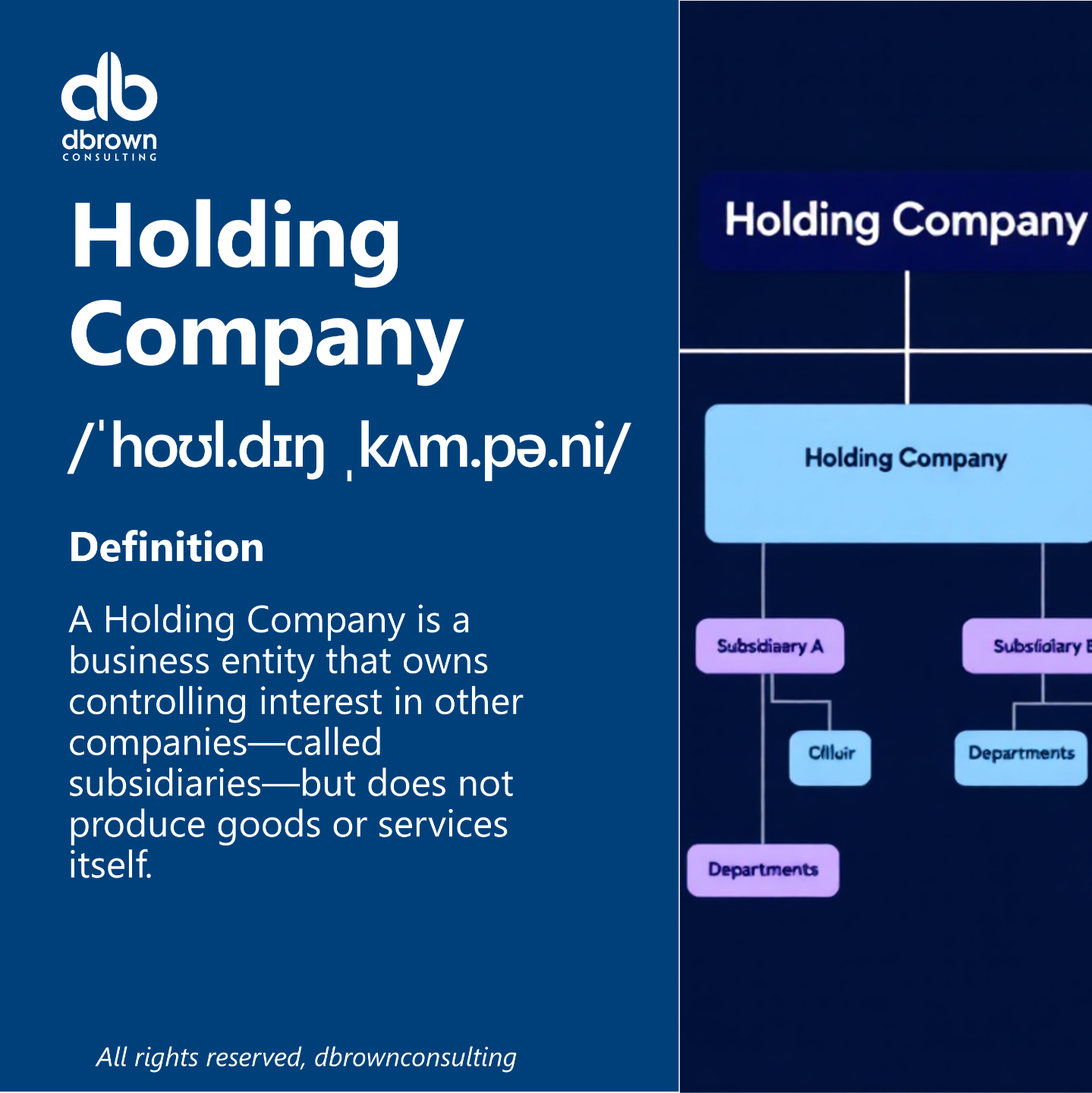

A Holding Company is a business entity that owns controlling interest in other companies—called subsidiaries—but does not produce goods or services itself. Its primary function is to control, manage, and protect investments in other businesses.

The holding company exercises ownership, governance, and sometimes strategic oversight over its subsidiaries but allows them to operate independently.

Origins

The legal and corporate concept of holding companies became formalized in the late 19th and early 20th centuries, particularly with the Sherman Antitrust Act (1890) in the U.S., and later the Public Utility Holding Company Act (1935). It was used by conglomerates and family offices to centralize control while minimizing risk and tax liabilities.

Usage

Industry Applications:

-

Conglomerates – E.g., Berkshire Hathaway holds stakes in insurance, railroads, and energy.

-

Private Equity – Funds often use a holding structure to manage multiple portfolio companies.

-

Family Businesses – For succession planning and asset protection.

-

Multinationals – Hold foreign subsidiaries through intermediate holding companies for tax optimization and regulatory compliance.

-

Startup Structures – To separate IP ownership from operational risk.

How Holding Company works

Structure:

A holding company:

-

Owns shares (typically >50%) of one or more subsidiaries.

-

May exert board control, but doesn’t manage day-to-day operations.

-

Can be structured as:

-

Pure holding company – Only holds investments.

-

Mixed holding company – Owns and operates a few business functions.

-

Legal and Financial Role:

-

Consolidates financial results of subsidiaries (as per GAAP/IFRS).

-

Limits liability exposure—subsidiary debt doesn’t directly affect the parent.

-

Enables tax planning, intercompany financing, and dividend flows.

Key Takeaways

-

A non-operational entity that owns and oversees subsidiaries.

-

Used for risk management, centralized control, and strategic investments.

-

Allows financial separation between business units.

-

Can enhance tax efficiency, especially in multinational structures.

-

Plays a crucial role in M&A, restructuring, and succession planning.

Types of Holding Companies

| Type | Description |

|---|---|

| Pure Holding Company | Sole purpose is ownership of other companies. |

| Mixed Holding Company | Owns companies and carries out limited operations. |

| Intermediate Holding Company | Positioned between the ultimate parent and operating subsidiaries (e.g., for tax/legal purposes). |

| Bank Holding Company | A specific regulatory entity under U.S. law to own and control banks (regulated by the Fed). |

Holding Companies & Financial Modeling

In financial models:

-

Consolidated Statements:

-

Combine subsidiary income, assets, and cash flows.

-

-

Minority Interest (NCI):

-

Represented if holding <100% of a subsidiary.

-

-

Dividends Received:

-

Modeled as intercompany cash inflows.

-

-

Debt Structuring:

-

Modeled separately to reflect non-recourse or ring-fenced financing at subsidiary level.

-

-

Tax Shielding:

-

Model intercompany interest and dividend flows to reflect holding company tax planning.

-

Nuances & Complexities

-

Limited Liability: The holding company is not liable for subsidiary debts, unless explicitly guaranteed.

-

Control Without Integration: Maintains operational independence across subsidiaries.

-

Regulatory Complexity: Some countries have anti-holding company rules to prevent monopolies or excessive tax deferral.

-

Cross-Shareholding Risks: Complexity in ownership can obscure financial transparency.

-

Dividends vs. Operational Cash: Holding companies rely on subsidiary cash flows to fund operations or service debt.

Mathematical Formulas

1. Consolidation Equation:

2. Equity Value of Holding:

3. Dividend Flow to Parent:

Master Financial Modeling with the FMA

Change your career today by earning a Globally Recognized Accreditation

Develop real-world financial modeling skills, gain industry-recognized expertise, stand out and start earning more by gaining the Advanced Financial Modeler (AFM) designation from the Financial Modeling Institute.

Our expert-led online cohort based program covers everything you need to become a world class financial modeling pro and advance your career in finance.

Related Terms

-

Subsidiary

-

Minority Interest (NCI)

-

Consolidated Financial Statements

-

Parent Company

-

Spin-Off

-

Bank Holding Company

-

Vertical Integration

-

Asset Protection Structure

References & Sources

Unlock the Language of Finance!

Elevate your financial acumen with DBrown Consulting’s exclusive newsletter. We break down complex finance terms into clear, actionable insights—empowering you to make smarter decisions in today’s markets.

Subscribe Today & Make Financial Jargon Simple!

We won't send spam. Unsubscribe at any time.