LOAN COVENANT

Definition

A loan covenant is a clause in a loan agreement that imposes certain conditions, restrictions, or requirements on the borrower to protect the lender’s interests. These covenants can be affirmative (requiring specific actions), negative (restricting certain actions), or financial (mandating specific performance metrics).

If the borrower violates a covenant, it may trigger a default, allowing the lender to demand immediate repayment, increase interest rates, or take other protective measures.

Origins

The term "covenant" comes from the Latin convenire (“to agree” or “come together”) and entered English through Old French. In finance, covenants evolved from early bond agreements where lenders imposed rules to safeguard repayment.

Usage

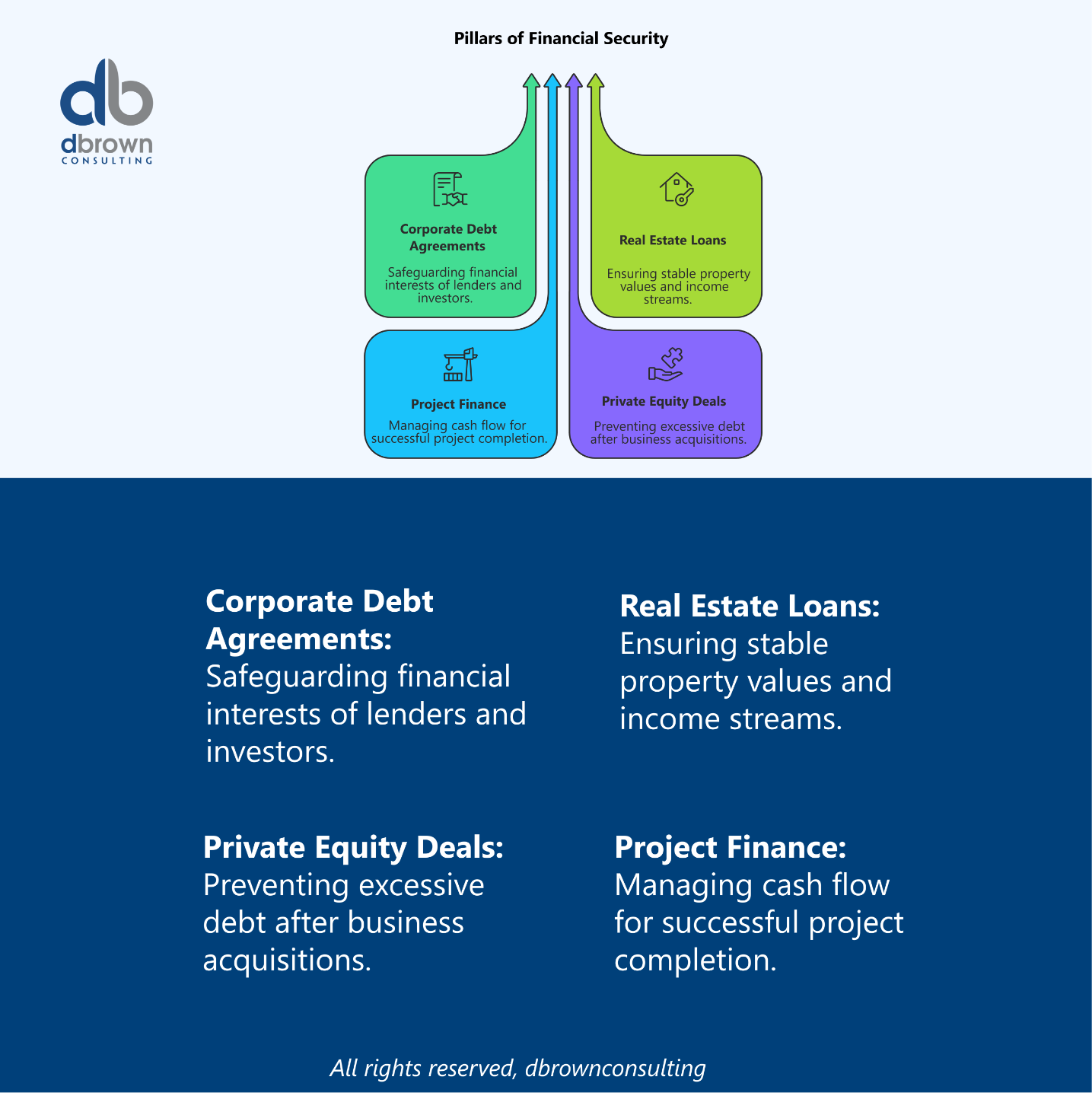

Loan covenants appear in:

-

Corporate debt agreements – Protecting banks and bondholders.

-

Real estate loans – Ensuring property value and income levels.

-

Project finance – Controlling cash flow allocations.

-

Private equity deals – Preventing over-leverage post-acquisition.

How Loan Covenants Works

When lenders issue loans, they include contractual promises to:

- Ensure the borrower remains financially healthy.

-

Restrict high-risk actions.

-

Provide early warnings of potential repayment problems.

Covenants are monitored periodically, often quarterly or annually, through borrower-provided financial statements and compliance certificates.

Types of Loan Covenants

1. Affirmative Covenants (Positive Covenants)

Borrower must do certain things:

- Maintain adequate insurance.

- Submit audited financial statements on time.

- Comply with applicable laws and regulations.

- Maintain a minimum level of working capital.

2. Negative Covenants (Restrictive Covenants)

Borrower must not take certain actions:

-

Take on additional debt above a certain threshold.

-

Pay dividends beyond an agreed limit.

-

Sell significant assets without lender approval.

-

Merge or acquire without consent.

3. Financial Covenants

Borrower must meet specific financial metrics:

-

Leverage Ratio:

-

Interest Coverage Ratio:

-

Current Ratio:

Key Takeaway

-

Loan covenants protect lenders by controlling borrower risk.

-

They can be positive, negative, or financial in nature.

-

Breaching a covenant can lead to penalties, renegotiations, or default.

-

Lenders monitor compliance regularly.

Context in Financial Modeling

Loan covenants are incorporated in:

-

Debt schedules – Ensuring projected financials stay within covenant limits.

-

Scenario analysis – Stress-testing if adverse events cause covenant breaches.

-

LBO models – Monitoring leverage and coverage ratios post-acquisition.

-

Credit agreements – Setting triggers for refinancing or restructuring.

Nuances & Complexities

-

Covenant Lite Loans: Loans with minimal restrictions, popular in high-liquidity markets.

-

Materiality Thresholds: Some covenants only trigger if breaches are above a certain level.

-

Negotiation Power: Strong borrowers can negotiate looser covenants.

-

Financial Statement Definitions: Lenders may define EBITDA or debt differently for covenant purposes.

Mathematical Formulas

While not a single formula, loan covenant compliance often involves ratio testing, such as:

-

Leverage Ratio Test:

-

Fixed Charge Coverage Ratio:

-

Minimum Liquidity Requirement:

Master Financial Modeling with the FMA

Change your career today by earning a Globally Recognized Accreditation

Develop real-world financial modeling skills, gain industry-recognized expertise, stand out and start earning more by gaining the Advanced Financial Modeler (AFM) designation from the Financial Modeling Institute.

Our expert-led online cohort based program covers everything you need to become a world class financial modeling pro and advance your career in finance.

Related Terms

-

Debt Agreement

-

Default

-

Leverage Ratio

-

Interest Coverage Ratio

-

Covenant Lite (Cov-Lite) Loans

-

Credit Risk

Real-World Applications

Example 1: Corporate Loan

A company’s $200M term loan includes:

-

Max Debt/EBITDA: 4.0×

-

Min Interest Coverage: 3.0×

-

Dividend cap of $5M/year

Example 2: Real Estate Loan

A commercial property mortgage requires:

-

Loan-to-Value (LTV) ratio ≤ 70%

-

Debt Service Coverage Ratio (DSCR) ≥ 1.25×

Example 3: Private Equity

In an LBO, financial covenants ensure leverage declines over time, preventing over-exposure for lenders.

References & Sources

Unlock the Language of Finance!

Elevate your financial acumen with DBrown Consulting’s exclusive newsletter. We break down complex finance terms into clear, actionable insights—empowering you to make smarter decisions in today’s markets.

Subscribe Today & Make Financial Jargon Simple!

We won't send spam. Unsubscribe at any time.