OPTION

Definition

An option is a financial derivative that gives the buyer the right—but not the obligation—to buy or sell an underlying asset (like a stock, bond, commodity, or index) at a specified price (strike price) before or at a certain expiration date.

A Call Option grants the right to buy.

A Put Option grants the right to sell.

The buyer pays a premium to the seller (writer) for this right. The seller assumes the obligation if the buyer exercises the option.

Origins

Options trace back to ancient Greece, where philosopher Thales used a primitive form of options to secure olive presses. Modern options gained structure in the 17th-century Amsterdam stock exchange and evolved into regulated instruments with the establishment of the Chicago Board Options Exchange (CBOE) in 1973.

The Black-Scholes model, introduced in the same year, formalized options pricing and revolutionized derivatives trading.

Usage

Financial Industry Applications

-

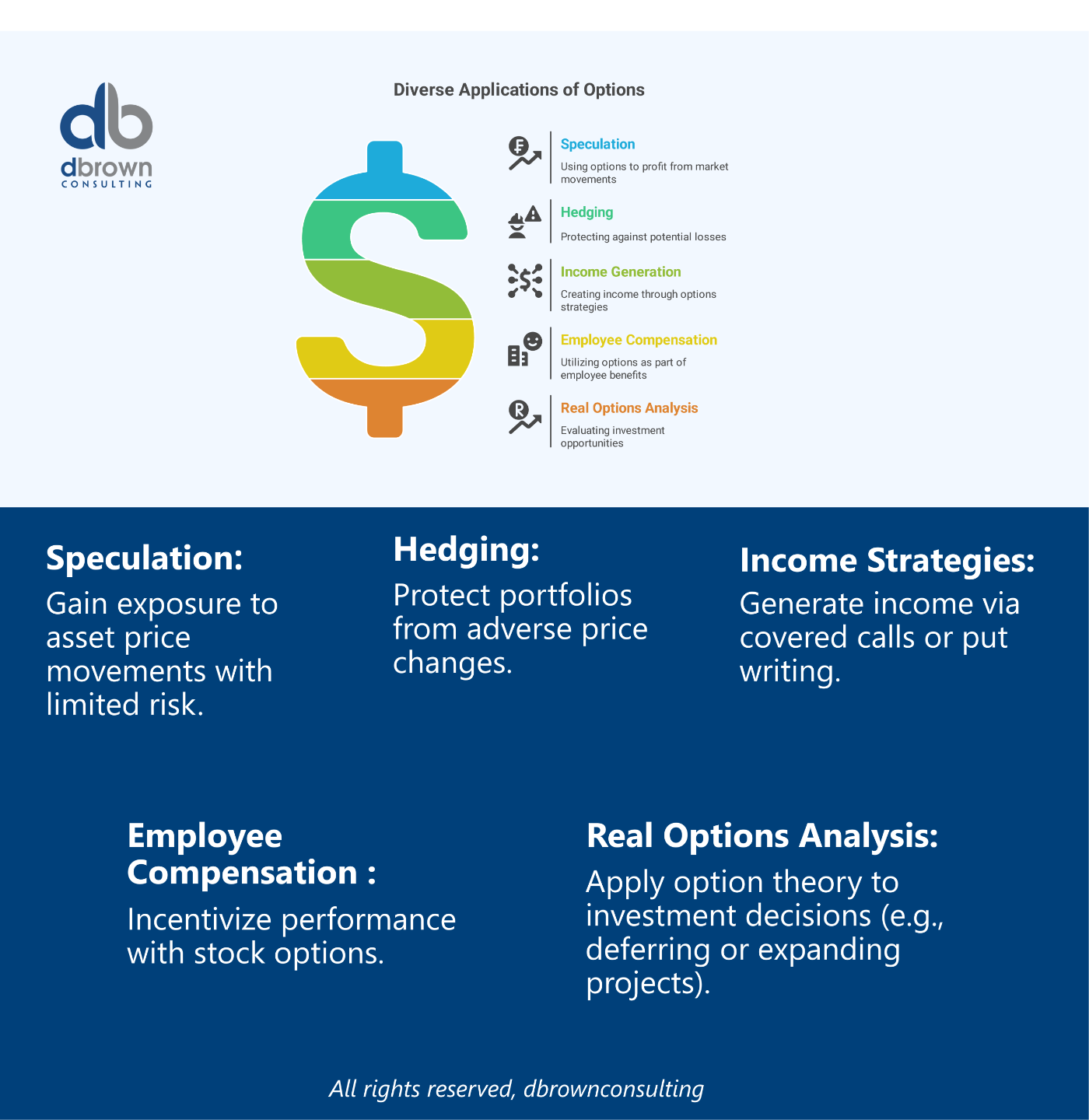

Speculation – Gain exposure to asset price movements with limited risk.

-

Hedging – Protect portfolios from adverse price changes.

-

Income Strategies – Generate income via covered calls or put writing.

-

Employee Compensation – Incentivize performance with stock options.

-

Real Options Analysis – Apply option theory to investment decisions (e.g., deferring or expanding projects).

How Option Works

| Term | Description |

|---|---|

| Underlying Asset | The asset the option is based on (e.g., stock, bond, commodity). |

| Strike Price | The price at which the asset can be bought or sold. |

| Premium | The cost paid by the buyer to the seller for the option. |

| Expiration Date | The last date on which the option can be exercised. |

| Moneyness | Whether the option is In, Out, or At the Money. |

Key Takeaway

-

Options are flexible, leveraged, and risk-controlled instruments.

-

They can be used for protection (hedging) or amplification (speculation).

-

Offer non-linear payoffs (e.g., asymmetry in potential gain/loss).

-

Require strong understanding of volatility, time decay, and greeks.

Types of Option

| Category | Subtypes |

|---|---|

| By Position | Call, Put |

| By Style | American, European, Bermudan |

| By Structure | Vanilla, Exotic (e.g., barrier, Asian, lookback) |

| By Market | Exchange-traded, Over-the-counter (OTC) |

| By Use Case | Financial Options, Real Options, Employee Stock Options |

Context in Financial Modeling

Options are essential in:

-

Valuation Models (e.g., Black-Scholes, Binomial Tree)

-

Risk Management – Modeling exposure via Greeks.

-

Real Options Analysis – Flexibility in capital budgeting.

-

Equity Compensation Accounting – Modeled under IFRS 2 / ASC 718.

Greeks in Modeling:

-

Delta: Sensitivity to price.

-

Gamma: Sensitivity of delta.

-

Theta: Time decay.

-

Vega: Sensitivity to volatility.

-

Rho: Sensitivity to interest rates.

Nuances & Complexities

-

Implied Volatility (IV): Forward-looking measure from option prices—key to valuation.

-

Time Decay: Option value erodes as expiration nears (Theta).

-

Liquidity & Slippage: Important for execution strategies.

-

Assignment Risk: Especially with American-style options.

Mathematical Formulas

1. Black-Scholes (European Call Option):

Where:

-

: Current price

-

: Strike price

-

: Risk-free rate

-

: Time to expiration

-

: Cumulative normal distribution

-

: Volatility

2. Put-Call Parity (European Options):

Master Financial Modeling with the FMA

Change your career today by earning a Globally Recognized Accreditation

Develop real-world financial modeling skills, gain industry-recognized expertise, stand out and start earning more by gaining the Advanced Financial Modeler (AFM) designation from the Financial Modeling Institute.

Our expert-led online cohort based program covers everything you need to become a world class financial modeling pro and advance your career in finance.

Related Terms

-

Futures

-

Warrants

-

Swaps

-

Volatility

-

Derivatives

-

Delta Hedging

-

Covered Call

-

Protective Put

Real-World Applications

1. Hedging Portfolio Risk

An investor holding a stock buys a put option to protect against downside risk.

2. Generating Income

A shareholder sells covered calls to earn premium income while holding the underlying stock.

3. Startup Compensation

Employees receive stock options at a fixed strike price, incentivizing long-term company value creation.

4. Real Options in Capital Budgeting

A mining company evaluates a project where it can delay development—modeled as a call option on project NPV.

References & Sources

Unlock the Language of Finance!

Elevate your financial acumen with DBrown Consulting’s exclusive newsletter. We break down complex finance terms into clear, actionable insights—empowering you to make smarter decisions in today’s markets.

Subscribe Today & Make Financial Jargon Simple!

We won't send spam. Unsubscribe at any time.