RATIO ANALYSIS

Definition

Ratio Analysis is a quantitative method of evaluating the financial performance, health, and efficiency of a business by examining the relationships between line items in its financial statements. Ratios provide insights into liquidity, profitability, solvency, efficiency, and valuation, making them essential tools for investors, creditors, analysts, and managers.

Origins

In accounting and finance, the systematic use of ratios began to emerge in the early 20th century, gaining wider adoption as analysts sought to assess corporate performance and risk more effectively.

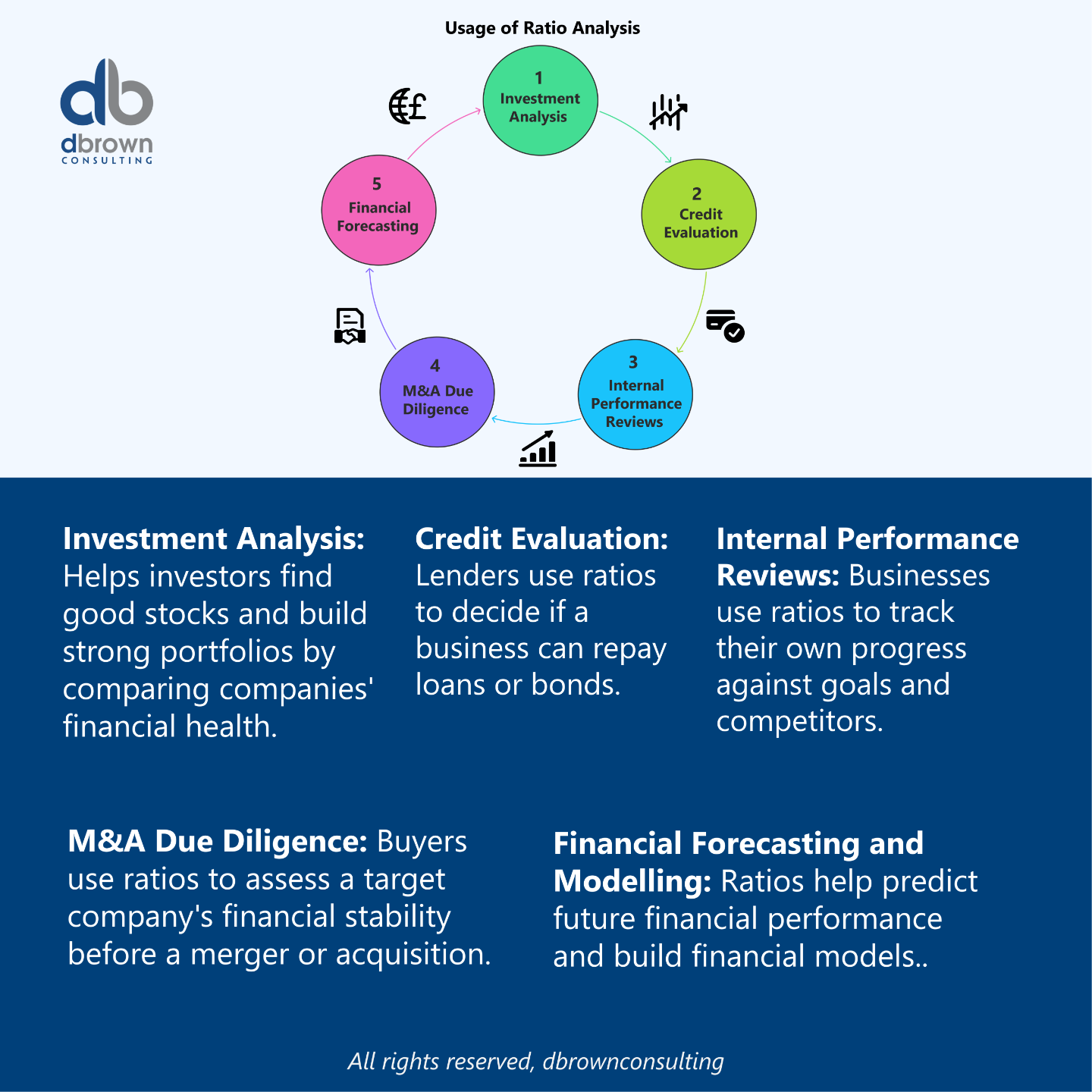

Usage

Ratio analysis is widely used in:

-

Investment analysis (e.g., stock screening, portfolio construction).

-

Credit evaluation (e.g., loan approvals, bond ratings).

-

Internal performance reviews (e.g., benchmarking, KPIs).

-

M&A due diligence (to assess the target's financial health and identify potential synergies).

-

Financial forecasting and modeling.

How Ratio Analysis Works

Ratio analysis involves calculating and interpreting ratios by dividing one financial metric by another to identify trends, strengths, and weaknesses.

Five Main Categories of Ratios:

-

Liquidity Ratios – Can the firm meet short-term obligations?

-

Profitability Ratios – Is the firm generating profit efficiently?

-

Solvency (Leverage) Ratios – Can the firm meet long-term obligations?

-

Efficiency (Activity) Ratios – How effectively are assets managed?

-

Valuation Ratios – How is the market pricing the company?

Key Takeaway

-

Ratio analysis translates raw financial data into actionable insights.

-

It enables comparative analysis across time periods and peer companies.

-

It identifies operational weaknesses, credit risks, and valuation gaps.

-

Ratios vary by industry and company size; context is critical.

Types of Financial Ratios

1. Liquidity Ratios

Measure the ability to meet short-term obligations.

-

Current Ratio:

-

Quick Ratio (Acid-Test):

-

Cash Ratio:

2. Profitability Ratios

Assess the firm’s ability to generate earnings.

-

Gross Margin:

-

Operating Margin:

-

Net Profit Margin:

-

Return on Assets (ROA):

-

Return on Equity (ROE):

3. Solvency (Leverage) Ratios

Measure long-term financial stability and debt levels.

-

Interest Coverage Ratio:

-

Debt-to-Equity Ratio:

-

Debt Ratio:

4. Efficiency (Activity) Ratios

Evaluate how effectively a firm uses its resources.

-

Inventory Turnover:

-

Receivables Turnover:

-

Asset Turnover:

-

Days Sales Outstanding (DSO):

5. Valuation Ratios

Used by investors to assess company value relative to price.

-

Price-to-Earnings Ratio (P/E):

-

Price-to-Book Ratio (P/B):

-

EV/EBITDA:

-

Dividend Yield:

Context in Financial Modeling

Ratio analysis is central to:

-

DCF and Comparable Company Analysis

-

Credit risk modeling

-

Sensitivity analysis (e.g., how changes in margins affect ROE)

-

Scenario planning and covenant testing

-

Investor presentations and pitch decks

Nuances & Complexities

-

Seasonality: Ratios can vary significantly by quarter.

-

Accounting Methods: Differences in depreciation or revenue recognition affect comparability.

-

Industry Benchmarks: A “good” ratio in one industry may be poor in another.

-

One-Off Items: Extraordinary gains/losses can distort ratios.

Master Financial Modeling with the FMA

Change your career today by earning a Globally Recognized Accreditation

Develop real-world financial modeling skills, gain industry-recognized expertise, stand out and start earning more by gaining the Advanced Financial Modeler (AFM) designation from the Financial Modeling Institute.

Our expert-led online cohort based program covers everything you need to become a world class financial modeling pro and advance your career in finance.

Related Terms

-

Common Sizing

-

Trend Analysis

-

Financial Ratios

-

DuPont Analysis

-

KPI (Key Performance Indicators)

Real-World Applications

Example 1: Equity Research

Analysts use profitability and valuation ratios to recommend buy/sell/hold ratings.

Example 2: Lending Decisions

Banks assess liquidity and leverage ratios before approving loans.

Example 3: Corporate Strategy

Executives use ratio trends to identify cost-saving opportunities or expansion readiness.

References & Sources

Unlock the Language of Finance!

Elevate your financial acumen with DBrown Consulting’s exclusive newsletter. We break down complex finance terms into clear, actionable insights—empowering you to make smarter decisions in today’s markets.

Subscribe Today & Make Financial Jargon Simple!

We won't send spam. Unsubscribe at any time.