CO SIGNER

Definition

A co-signer is a person who agrees to take equal responsibility for repaying a loan, lease, or other debt obligation alongside the primary borrower. If the borrower fails to make payments, the co-signer is legally obligated to fulfill the debt terms, including principal, interest, and any penalties.

Co-signers are often used when the primary borrower lacks sufficient credit history, income, or a strong credit score to qualify for a loan on their own.

Origins

The term "co-signer" comes from the Latin signare (“to sign”), with the prefix "co-" meaning “together.” In legal and financial contexts, it refers to two or more parties signing a contractual agreement together, sharing liability. The modern use became common with the rise of consumer credit and formalized lending agreements in the 20th century.

Usage

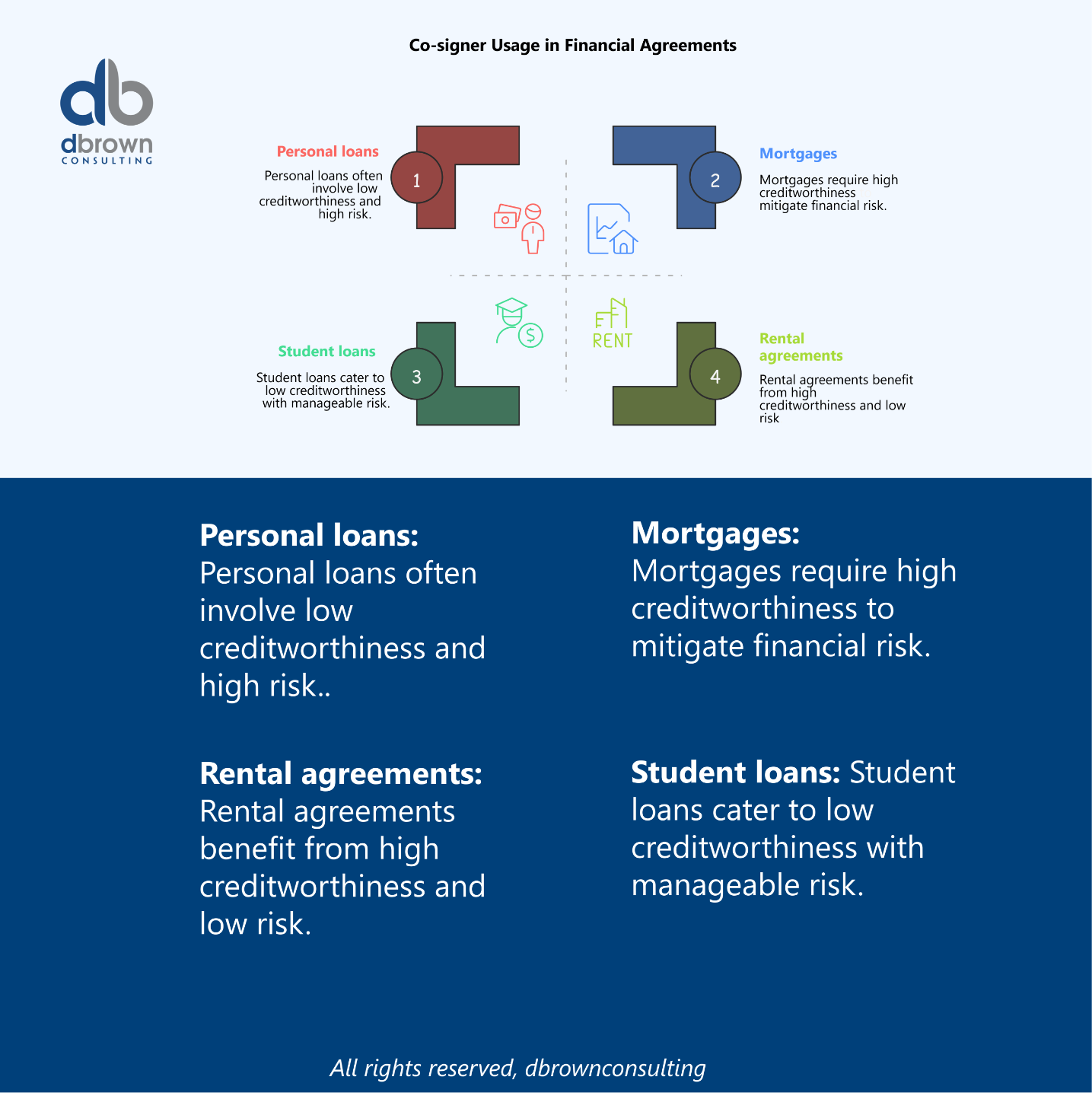

Co-signers are common in:

-

Personal loans – Helping someone with limited credit get approved.

-

Auto loans – Ensuring financing for younger or first-time buyers.

-

Student loans – Allowing students without income to secure education financing.

-

Rental agreements – Assuring landlords of rent payments.

-

Mortgages – Strengthening an application’s creditworthiness.

How a Co-Signer Works

-

Loan Application – Borrower applies for credit but may not qualify alone.

-

Co-Signer Added – Lender assesses the co-signer’s income, credit score, and debt profile.

-

Equal Responsibility – Both borrower and co-signer are legally bound to repay.

-

Default Consequences – If borrower misses payments, co-signer must step in.

-

Credit Impact – Payment history (positive or negative) appears on both parties’ credit reports.

Difference Between Co-Signer and Guarantor

-

Co-Signer: Shares immediate and equal responsibility for repayment from day one.

-

Guarantor: Responsible only if the borrower defaults and legal remedies have been exhausted.

Risks for Co-Signers

-

Credit Damage – Missed or late payments harm both credit profiles.

-

Debt-to-Income Ratio Impact – The loan counts toward the co-signer’s debt load, possibly affecting future borrowing capacity.

-

Legal Liability – Co-signer can be sued for repayment.

-

Relationship Strain – Money disputes can damage personal relationships.

Key Takeaway

-

A co-signer shares full legal responsibility for repayment.

-

Their credit and income are used to strengthen the borrower’s application.

-

Any missed payments impact both parties’ credit scores.

-

Co-signers often face collection efforts before the lender pursues the borrower.

Context in Financial Modeling

Co-signers are relevant for:

-

Consumer credit risk models – Reduced default probability with stronger credit profiles.

-

Loan underwriting criteria – Higher approval rates with co-signed applications.

-

Debt recovery scenarios – Co-signer liability included in recovery calculations.

Nuances & Complexities

-

Removal from Loan – Often requires refinancing without the co-signer.

-

Credit Reporting Rules – Any delinquency is reported to all signers.

-

Bankruptcy Impact – Borrower’s bankruptcy does not erase co-signer responsibility.

-

State Laws – Some jurisdictions have specific disclosure requirements for co-signers.

Mathematical Formulas

While there’s no single formula for co-signing, lenders often re-evaluate debt ratios with a co-signer:

Debt-to-Income (DTI) Calculation:

Adding a co-signer increases Gross Monthly Income, lowering the DTI and improving approval odds.

Master Financial Modeling with the FMA

Change your career today by earning a Globally Recognized Accreditation

Develop real-world financial modeling skills, gain industry-recognized expertise, stand out and start earning more by gaining the Advanced Financial Modeler (AFM) designation from the Financial Modeling Institute.

Our expert-led online cohort based program covers everything you need to become a world class financial modeling pro and advance your career in finance.

Related Terms

-

Guarantor

-

Primary Borrower

-

Joint Applicant

-

Loan Covenant

-

Creditworthiness

-

Debt-to-Income Ratio (DTI)

Real-World Applications

Example 1: Auto Loan

A parent co-signs a $20,000 car loan for their child. If the child stops making payments, the parent must repay the lender.

Example 2: Student Loan

A student with no income secures a private loan with a co-signer. Both parties’ credit histories will reflect repayment activity.

Example 3: Apartment Lease

A recent graduate rents an apartment with a parent as co-signer to satisfy the landlord’s income requirement.

References & Sources

Unlock the Language of Finance!

Elevate your financial acumen with DBrown Consulting’s exclusive newsletter. We break down complex finance terms into clear, actionable insights—empowering you to make smarter decisions in today’s markets.

Subscribe Today & Make Financial Jargon Simple!

We won't send spam. Unsubscribe at any time.